Africa Credit Rating Trends 2025 In Review: Divergence And Resilience

Key Takeaways

- Seven of our sovereign upgrades in Africa in 2025 were driven primarily by improving growth prospects and reform momentum.

- These upgrades had a ripple effect, leading us to take positive rating actions on financial and corporate entities in countries including Egypt, Morocco, and South Africa.

- While many countries saw improvements, we took negative rating actions on Botswana and Senegal to reflect specific challenges such as declining diamond prices and high debt. Also, institutional instability in Benin and Madagascar led us to revise our outlooks.

- Multilateral lending institutions (MLIs), supported by their strong creditworthiness, offer an anchor point for scalable blended finance amid persistent funding challenges.

Divergent credit narratives emerged in 2025 and led us to take various rating actions on African sovereigns. The main factors supporting our seven upgrades were improving growth prospects and favorable reform momentum. Additionally, fiscal improvements and diminishing liquidity pressures helped enhance credit profiles, and Ghana and Zambia made critical progress with debt restructuring under the G20 framework.

The year started with five sovereigns on positive outlooks. Four (Morocco, Egypt, South Africa, and Togo) upgrades followed, with Benin being the exception. The upgrades led directly or indirectly to similar positive rating actions across the financial and corporate sectors we cover in Egypt, Morocco, and South Africa. Similarly, our positive outlook on Nigeria led us to revise our outlooks on Nigerian banks in 2025. Our corporate rating actions also reflected the positive commodity cycle and structural reforms that underpinned stronger economic prospects in Morocco and Nigeria, as well as stronger fiscal outcomes in South Africa. We ended the year with South Africa, Cape Verde, Nigeria, and Uganda on positive outlook. Our negative rating actions were on Botswana and Senegal, reflecting depressed diamond prices and elevated debt stock, respectively. Political instability was evident in both Benin and Madagascar, leading us to revise our positive outlook to stable on the former, while we placed the latter on CreditWatch with negative implications. We recently removed our CreditWatch on Madagascar and assigned a stable outlook on the ‘B-’ long term rating.

Gradual Growth Amid An Uneven Regional Recovery

GDP growth was broadly stable in 2025, averaging 4.5% in 2025 and 2024. Economic growth across our rated sovereigns is expected to remain resilient, with stable average real GDP growth in 2026. This reflects ongoing economic reforms, easing inflationary pressures, and resilient domestic demand. However, growth remains uneven across regions and continues to fall short of the pace required for meaningful debt reduction and job creation.

Commodity dynamics contributed to rating changes. Weaker diamond prices have strained Botswana’s fiscal performance, while favorable prices for gold and cocoa have supported revenues and external balances in South Africa, Ghana, and Côte d'Ivoire. In several countries, robust export earnings, also underpinned by stronger export volumes, have strengthened foreign exchange reserves.

Africa’s limited global trade integration as well as tariff exemptions on key mineral exports have shielded the region from any severe economic fallout stemming from U.S. tariffs. Meanwhile USAID funding has proven more challenging to replace, leading to a shortfall that could exacerbate health vulnerabilities and slow poverty reduction.

Across the region, steady growth, lower inflation, and supportive commodity prices (excluding oil) along with a weaker U.S. dollar are likely to lower financing costs and help reform implementation (see “African Sovereign Ratings Outlook 2026: Positive Momentum Stabilizing,” Feb. 2, 2026).

U.S. dollar sovereign issuance dominated international capital markets in 2025

Some sovereigns accessed larger volumes at lower cost while others encountered elevated borrowing expenses, underscoring the diverse credit environment across Africa. Overall, the cost of funding in 2025 was 100 bps lower than in 2024, averaging 7.7% after considering currency swaps for Benin and Côte d’Ivoire bonds. Morocco's low euro rates also contributed to overall reduced funding costs, while other African sovereigns issued in U.S. dollars at higher rates. U.S. dollar bond issuance continued to dominate the international capital markets, reflecting a preference for dollar-denominated instruments. In 2025, African sovereigns raised about US$18 billion and €2 billion, up from $12.85 billion in 2024.

- Egypt opened the way after a hiatus of four years with nearly US$2 billion raised in two tranches in January at an average coupon of 9.04%, amid strong demand from investors for these fixed rate bonds. The government issued a dual tranche sukuk of $2.5 billion at an average of 7.16% with a shorter average duration of about five years compared to six-and-a-half years for the Eurobonds.

- South Africa raised $3.5 billion at an average coupon of 6.69% and longer average duration of 21 years.

- Midsize issuers Angola and Côte d’Ivoire each raised $1.75 billion, at a similar coupon as Egypt for Angola and at 6.4% for Côte d’Ivoire due to the euro-dollar currency swap. Nigeria issued a total of US$2.35 billion through a dual tranche transaction with a 10-year at 8.625% and a 20-year maturity at 9.125% structure. Kenya executed two separate dual-tranche issuances for a total ofUS$3 billion to extend maturities and ease refinancing risks. Congo and Benin went to the market with small issuances; the former reached a nearly 10% coupon for a seven-year issuance after 20 years of absence, while the latter had a dollar-euro swap for three years at 6.48% compared to an initial coupon of 8.375%, with a 16-year duration. This reflects Benin’s stronger market access and investor confidence.

- Morocco is the only sovereign raising €2 billion at about 4.3% with an average duration of seven years. This is the lowest coupon for this dual tranche Eurobond. Morocco continues to fund its infrastructure projects while reducing currency risk by issuing in euros, consistent with its strong trade linkages with the EU.

Improved global credit conditions and a stronger track record with international investors enabled Benin to issue bonds in January 2026, combining a $350 million Eurobond (2038) fully hedged in euros at 6.19% with its inaugural international sukuk. This raised $500 million over seven years at 4.92% and drew orders totaling $7 billion, highlighting significant interest from Islamic investors in Africa. As the sukuk market continues to slowly expand in Africa, we expect other African sovereigns will follow. Nigeria is a frequent issuer in its domestic market and is eyeing its first $500 million international sukuk in 2026.

Sustainable bonds and loans volumes have moderated markedly in 2025, with very few sovereigns issuing after the $13 billion raised in 2024. Governments shifted focus to funding allocations from previous issuances and slightly toward sustainability-linked loans. Côte d’Ivoire secured a $0.5 billion sustainability-linked loan and Nigeria raised a green bond in its domestic market, raising Nigerian naira (NGN) 50 billion in June 2025. Green bond issuance increased in 2025 compared to 2024 with issuers from Mauritius and South Africa leading the way. For the first time, Industrial Development Corporation of South Africa issued a ZAR3.4 billion sustainable bond in two tranches, while Nedbank issued a ZAR2.5 billion social bond in December 2025 with African Development Bank’s (AfDB’s) support. AfDB returned to the market with a €500 million green bond in 2025. Regional governments entered the field with the state of Lagos issuing nearly NGN15 billion in 2025, albeit modest compared to the ZAR1 billion green bond issued by the city of Cape Town in 2017.

Sovereign Ratings Overview

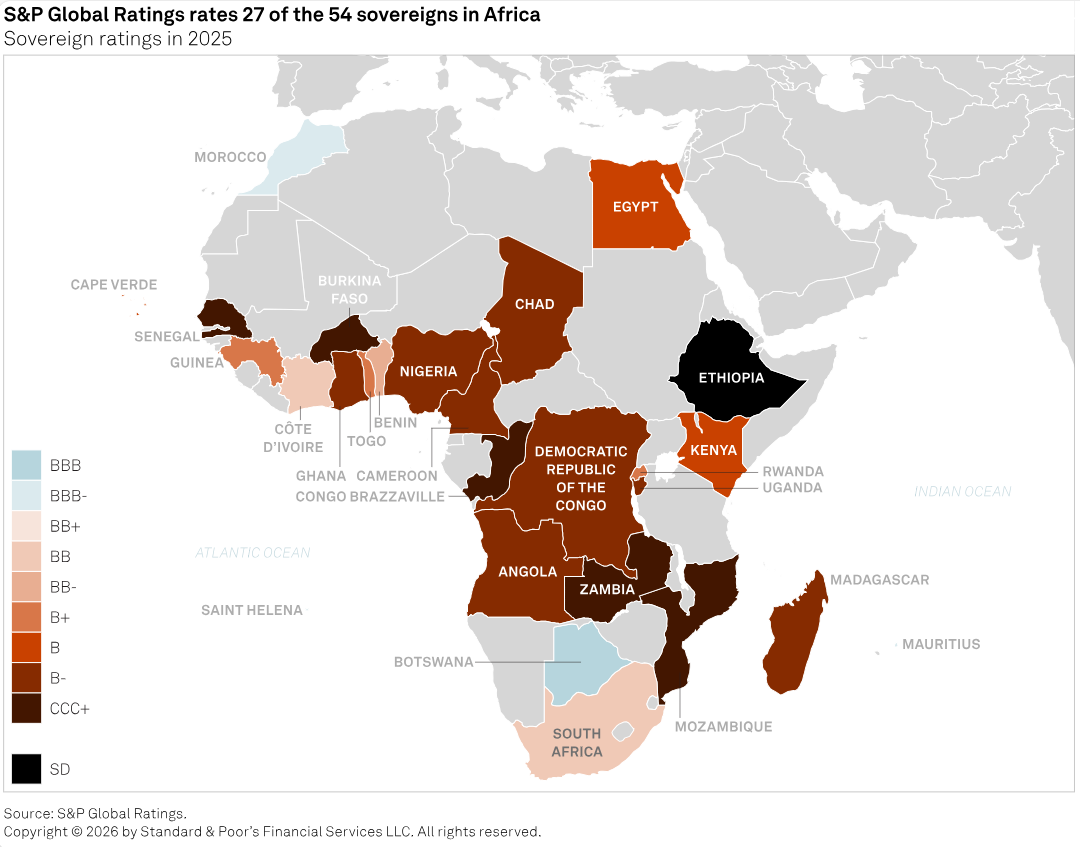

Of the 54 sovereigns in Africa, we publicly rate 27. We expanded our rating universe in the region when we assigned 'B+/B' long-and short-term ratings to the Republic of Guinea, in 2025.

In 2025, the number of investment-grade sovereigns increased to four, from three, with ratings in the ‘BBB’ category--Botswana at ‘BBB’ and Morocco, Mauritius, and St Helena all at ‘BBB-’.

Half our African sovereign credit ratings are in the 'B' category, while fewer than a quarter are in the 'BB' category or above. The sovereigns we rate 'B' or 'B-' tend to be concentrated in Middle Africa. Ethiopia remains the only African sovereign whose foreign currency rating is selective default (‘SD’) at year-end 2025 because it has yet to reach an agreement with bondholders on its $1 billion Eurobond due 2024. Ghana and Zambia are no longer ‘SD’ now that they’ve completed their debt restructuring under the G20 framework. Our local currency rating on Mozambique is also ‘SD’ due to ongoing domestic debt exchanges that we deem to be distressed.

Sovereign Rating Snapshots: Rating Actions

- Positive rating actions reflected progress on economic and fiscal reforms, advances in structural reform agendas, and steps toward debt restructuring, collectively strengthening sovereign creditworthiness.

- Nevertheless, challenges remain uneven, with some sovereigns facing economic and fiscal constraints including liquidity pressures, which continue to weigh on their credit profiles.

Most of our positive rating actions were upgrades rather than outlook revisions. We upgraded Morocco to ‘BBB-’, restoring the investment grade status it lost in 2021 amid the pandemic and other shocks. We also upgraded Egypt, Kenya, Togo, Zambia, Ghana, and South Africa. Our underlying rationales differ. Some sovereigns have benefitted from structural reforms that have led to stronger economic prospects (Morocco, Egypt, Togo) and lower external imbalances (Kenya), as well as better fiscal trajectories (South Africa) while others made progress on their debt restructuring (Ghana and Zambia).

Four out of our seven negative rating actions were downgrades to Botswana (once) and Senegal (on three occasions). We lowered our ratings on Botswana by one notch because of the impact of lower diamond prices and fiscal and external imbalances. We downgraded Senegal by three notches from ‘B+’ to ‘CCC+’ following underreported public debt and subsequent rising fiscal pressures.

Rating Actions: Sovereigns

| Ratings Snapshots | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Upgrades | |||||||||||

| Togo | Kenya | Morocco | Egypt | ||||||||

| B+/Stable/B | B/Stable/B | BBB-/Stable/A-3 | B/Stable/B | ||||||||

| In April 2025, we raised our rating by one notch to 'B+', driven by our expectation that Togo will deliver on economic and fiscal reforms, including by mobilizing tax revenue. | In August 2025, we raised our rating by one notch to 'B', reflecting reduced near-term external liquidity risks as robust export earnings and strong diaspora remittances continued to strengthen Kenya’s FX reserves. | In September 2025, we upgraded Morocco by one notch to 'BBB-' because of its solid economic performance and improved outlook supported by a sound policy mix and strong structural, socioeconomic, and budgetary reform momentum. We assume these factors will continue to further formalize and diversify the economy. | In October 2025, we upgraded Egypt from 'B-' to 'B', reflecting ongoing reforms and stronger growth. The shift to a flexible exchange rate has boosted tourism and remittances, while the government posted a primary surplus of 3.5% of GDP for fiscal 2025. | ||||||||

| South Africa | Ghana | Zambia | |||||||||

| BB/Positive/B | B-/Stable/B | CCC+/Stable/C | |||||||||

| In November 2025, we raised our rating by one notch to 'BB', supported by strengthening GDP growth driven by reforms in the electricity and other sectors. With improving tax collections and expenditure controls, we expect fiscal consolidation will continue through 2028 alongside a reduction in contingent liabilities largely tied to performance improvements at state-owned electricity utility, Eskom. | In November 2025, we raised our rating by one notch from ‘CCC+’ as rising export volumes and favorable prices for key exports—gold and cocoa—supported the Ghanaian cedi and boosted gross foreign-currency reserves, thereby improving fiscal performance and the balance of payments. Earlier, in May, we had raised our rating by one notch from ‘SD’ as the authorities’ steps to restructure the remaining commercial debt, following the October 2024 Eurobond exchange, alongside falling inflation, better reflected Ghana’s improving creditworthiness. | In November 2025, we upgraded Zambia by one notch from ‘SD’, reflecting improved creditworthiness driven by the authorities’ recent steps to restructure remaining commercial debt, as well as favorable market conditions that supported a ramp-up in copper production. | |||||||||

| Downgrades | |||||||||||

| Senegal | Botswana | ||||||||||

| B/Negative/B | B-/Negative/B | CCC+/Watch Dev/C | BBB/Negative/A-2 | ||||||||

| In February 2025, we lowered our long-term rating to ‘B’ from ‘B+’, with a negative outlook, following significant revisions to fiscal and debt data, which revealed a fundamentally weaker picture. We expect fiscal deficits will gradually adjust but still average around 6.5% of GDP in 2025-2028, while debt remains near 100% of GDP, constraining fiscal flexibility. | In July 2025, we lowered Senegal to ‘B-’ because of higher financing needs. Debt revisions, high deficits, and arrears pushed borrowing above 25% of GDP, while external financing pressures could have complicated IMF negotiations. Despite strong growth, public finances remain constrained and vulnerable to shocks. | In November 2025, we downgraded Senegal to ‘CCC+’ and put it on CreditWatch developing. General government debt was an estimated 119% of GDP, over 40 percentage points higher than in December 2024. Despite steps to boost growth and tax collection, high debt and interest burdens have left public finances precarious, particularly without comprehensive official support. | In September 2025, we lowered our ratings by one notch to 'BBB' because of weaker diamond prices weighing on Botswana's minerals-dependent economy, fiscal revenue, and exports, as well as its deteriorating fiscal position in the absence of a significant policy adjustment. In March 2025, we revised our outlook to negative from stable on external and fiscal pressures. | ||||||||

| Outlook revisions | |||||||||||

| Benin | Mozambique | Cape Verde | Madagascar | ||||||||

| BB-/Stable/B | CCC+/Negative/C | B/Positive/B | B-/Watch Neg/B | ||||||||

| In December 2025, we revised our outlook to stable, from positive, on heightened security risks following a foiled coup, despite continued institutional resilience. We project GDP growth will remain strong at around 6.1% annually over 2025-2028, supported by ongoing fiscal reforms. However, the coup underscores rising security threats, which could strain political stability and increase security-related costs. | In February 2025, we assigned a negative outlook, which reflects ongoing liquidity pressures and lingering administrative shortcomings in Mozambique's debt management, alongside macroeconomic pressures. | In August 2025, we assigned a positive outlook, which reflects our expectation that Cape Verde’s fiscal and external fundamentals could improve more than we expect, reflecting rising growth and foreign currency earnings from its outsized tourism sector. | In October 2025, we placed Madagascar on CreditWatch negative, reflecting the significant political uncertainty that could undermine its growth prospects, delay fiscal consolidation efforts, and restrict access to official external financing. | ||||||||

| Nigeria | Uganda | Senegal | |||||||||

| B-/Positive/B | B-/Positive/B | CCC+/Watch Dev/C | |||||||||

| In November 2025, we assigned a positive outlook, highlighting our expectation that the monetary, economic, and fiscal reforms being implemented by the Nigerian authorities will yield positive benefits over the medium term. | In November 2025, we assigned a positive outlook, reflecting the potential for stronger growth and per capita income than we currently forecast, given favorable terms of trade and key oil projects that are set to commence in the next 12-18 months. | In November 2025, we placed Senegal on CreditWatch developing, signaling that we could lower our ratings if the government is unable to refinance its upcoming commercial maturities on time and in full. Conversely, rating upside could arise if Senegal refinances its upcoming maturities and implements a resolute budgetary consolidation. | |||||||||

Our outlook changes were slightly tilted to the negative, largely driven by Senegal, Mozambique, and Madagascar. We subsequently revised our outlook on Madagascar to stable in January 2026.

We revised to positive our outlooks on Nigeria, Uganda, and Cape Verde. Our outlook on South Africa remains positive. In late 2025 we revised our outlook on Benin to stable, from positive, following the foiled coup that illustrated the security challenges in the West African region.

MLIs Credit Profiles

- Robust policy mandates and strong balance sheets continue to drive MLIs in our portfolio. Our ratings are in the upper investment-grade category and range between 'A' and 'AAA'. All our outlooks are stable, except for Africa Finance Corporation (AFC), which has a positive outlook. The credit profiles of MLIs with a particular focus on Africa remained strong in 2025. In May, we upgraded BADEA to 'AA+', underpinned by its role and policy importance.

- Capital continues to support credit ratings as entities focus on risk-transfer and balance-sheet optimization to accelerate capital mobilization.

- MLIs play an increasing role in bridging funding gaps as African sovereigns face tight fiscal flexibility and seek innovative financing to build infrastructure.

- We continue to expand our coverage of MLIs. In January 2026, we rated AFC 'A' with a positive outlook.

| Ratings snapshots--MLIs and development banks | ||||

|---|---|---|---|---|

| African Development Bank | Arab Bank for Economic Development | Africa Trade & Investments Development Insurance | ||

| AAA/Stable/A-1+ | AA+/Stable/A-1+ | A/Stable/-- | ||

| Full Analysis | Rating Action | Full Analysis | ||

| The stable outlook indicates that we assume AfDB will expand lending in both its sovereign and non-sovereign portfolios. We anticipate that it will benefit from preferred creditor treatment and will maintain strong funding and liquidity profiles. We also anticipate that shareholders will demonstrate their support through timely capital payments and an ongoing willingness to provide extraordinary support if needed. | The stable outlook reflects our expectation that BADEA will sustain sound capitalization, with its high risk-adjusted capital ratio, and solid liquidity through conservative lending and a low, albeit increasing, reliance on debt. The outlook also balances our expectation that the bank's asset quality will remain strong, bolstered by diversified exposures and its rising role as a countercyclical lender in sub-Saharan Africa, against the risks associated with relatively low-rated sovereigns in the region. | The stable outlook reflects our view that despite growing regional stress and difficulties related to the reimbursement of claims in Niger and Ghana, ATIDI members will remain committed to upholding their preferred creditor treatment with the agency over the next 12-24 months. We expect ATIDI will continue to consolidate its role and relevance in Africa through underwriting and by expanding its shareholder base, while strengthening key managerial and risk functions that support its growth. | ||

| East African Development Bank | Africa Finance Corporation | |||

| A/Stable/A-1 | A/Positive/A-1 | |||

| Rating Action | Rating Action | |||

| The stable outlook reflects our view that EADB will deliver its policy mandate by increasing its footprint in member countries, while maintaining a robust financial profile. We anticipate that all sovereign member states will continue giving EADB preferred creditor treatment, as granted by the charter, and that nonperforming loans to the private sector will remain contained. We anticipate the bank’s risk management and governance will continue strengthening and upholding sound banking principles. | The positive outlook reflects our expectation that AFC will execute its strategy by further diversifying its shareholder structure and expanding its capital base, while sustaining strong capital and liquidity. | |||

S&P Global Ratings updated its criteria for rating MLIs (see "Multilateral Lending Institutions And Other Supranational Institutions Ratings Methodology," Oct. 13, 2025) with significant changes to risk weights for sovereigns and the single-name concentration charge for sovereign exposures as new data sets and studies have enabled a more robust calibration of the risks. The recalibration affects sovereign exposures rated 'BB-' or below that have demonstrated a robust repayment track record vis-a-vis the MLIs. As previously noted, a large cohort of our rated African sovereigns would fall under this category and therefore, all else being equal, lending to African sovereigns would require less capital for MLIs, which should enable more lending. While other constraints, both external and internal, remain and would need to be addressed, we estimate our criteria change could facilitate $600 billion-$800 billion in new sovereign loans globally for the sector. Considering Africa’s share of lending, a simple calculation assuming an equal split of new capacity could yield $90 billion-$120 billion in additional lending to the continent.

MLIs play a crucial role in the development agenda of African economies because of their capacity to mobilize capital and pioneer funding structures. They are moving toward an originate-to-distribute model as they seek to optimize their capital. AfDB recently launched a synthetic securitization platform with the objective of de-risking its balance sheet by pooling and transferring credit risks stemming from existing loans to other investors against a premium. Another key initiative is Mission300, launched jointly by AfDB and the World Bank, which aims to provide electricity to 300 million people on the continent by 2030 through investments in renewables, mini grids, and grids. This global initiative has onboarded other MLIs and has the buy-in from governments to commit to sectoral reforms. While the shortage of first-loss concessional and private capital persists, global initiatives offer an impetus to create stronger public-private partnerships and are a catalyst for blended finance, both of which ultimately provide paths to de-risk and recycle capital at scale.

Rating Actions: Non-Sovereign Africa-Based Entities

Improved macroeconomic conditions also supported the private sector, underpinning sound business prospects and strengthening credit metrics.

Our non-sovereign rating universe has about 50% of issuers rated 'BB-' and above, while nearly one quarter are anchored at 'BB' and 'B-'. The cohort includes South African banks, insurers, and corporates as well as Nigerian financial institutions, where we have the highest number of ratings. Egyptian and Tunisian banks are concentrated in the 'B' category because of our view of the related sovereign creditworthiness while Moroccan banks tend to be in the 'BB' category, below the Moroccan sovereign. That said, we rate certain corporate and insurance entities in South Africa above the foreign currency sovereign rating due to their ability to pass our hypothetical sovereign default stress test, which demonstrates that they maintain sufficient capital and liquidity.

Our positive outlook distribution is underpinned by the positive outlooks on Nigerian and South African banks.

Rating Actions: Financial Institutions

Our coverage of banks in Morocco, Egypt, Nigeria, and South Africa accounts for the majority of respective domestic system assets. Except for Morocco, our ratings on financial institutions are generally constrained by those on their sovereigns due to the direct and indirect interconnectedness between banks and sovereign creditworthiness. We rate South African and Moroccan banks in the ‘BB’ category while Nigeria, Tunisian, and Egyptian banks are in the ‘B’ category.

That said, last year we raised our global and national scale ratings on eight South African banks and maintained our positive outlooks, supported by improving economic and fiscal trajectories in the country. Similarly, we raised our ratings on Egyptian banks following our sovereign upgrade because we anticipate the stronger economic environment will benefit banks’ financial performances.

In Morocco, we rate about 60% of the system assets that are concentrated at the top-tier banks. In October we raised our rating on Attijariwafa Bank, reflecting its stronger financial performance.

Positive and stable outlooks are broadly evenly split, and two entities have negative outlooks. In Nigeria, we revised our outlooks on seven Nigerian banks to positive from stable and affirmed our global scale ratings on the banks. We maintained stable outlooks on three entities. We also maintained a positive outlook on the South African banks we rate, reflecting the positive outlook on the sovereign.

We revised our rating outlook on Togo-based Ecobank Transnational Inc. to negative due to the deteriorating creditworthiness of its subsidiary Ecobank Nigeria Ltd, which could affect ETI’s reputation and credit profile, constraining its market access and compressing its liquidity.

Rating Actions: Fixed Income Funds

We rate one fixed income fund in Morocco. We raised our rating on Upline Tresorerie Fund by several notches to 'A-f' from 'BB+f', reflecting the stronger underlying creditworthiness of its investments following the sovereign upgrade to investment grade. At the same time, we placed the 'A-f' rating on CreditWatch with positive implications, reflecting the potential revision of the fund's duration strategy following the upgrade of Morocco to ‘BBB-.’

In 2025, we withdrew our ratings on four South African fixed income funds at the sponsors’ request. At the time of the withdrawal, our South African national scale ratings on the funds ranged between 'zaAA-' and 'zaAAAf'.

Rating Actions: Corporates

We have public global scale ratings on 28 corporates. In 2025, we assigned our 'BBB-' long-term rating to Valterra Platinum Ltd., a leading platinum group metals miner in South Africa, and our 'B' long-term rating to Ivanhoe Mines Ltd, a leading midsize copper miner. We assigned our 'zaAAA/zaA-1+' South Africa national scale ratings to Germany-based truck manufacturer TRATON SE, reflecting our 'BBB' long-term global scale rating on TRATON, a subsidiary of VW. Puma International Financing S.A., a distributor of refined oil products across 35 African countries, is another recent rating, at ‘BB’.

Our corporate rating actions were mostly on South African companies, in particular government-related entities (GREs). GRE ratings are influenced by their stand-alone credit profiles as well as our assessments of the likelihood of extraordinary government support from the related sovereign, as well as our rating on the sovereign. Currently our ratings on two South African GREs (Rand Water and Telkom SA SOC) are on positive outlook, in line with South Africa. Four corporates recorded an upgrade following a previous positive outlook revision, including OCP in Morocco when we equalized our ratings with the sovereign ratings. Changes in country and industry risks together with moderating financial risks led us to upgrade some pan-African telecommunication companies. We rate one company, Tullow Oil PLC, in the ‘CCC’ category because of debt restructuring risk in the context of moderate oil prices. We also upgraded Côte d’Ivoire Energies to 'BB-', one notch below the sovereign, supported by the budgetary mechanism provided by the government.

Our corporate outlook distribution is tilted to the positive with more stable and positive outlooks combined in 2025 (82%) compared with 2024 (75%). As of year-end 2025, we had placed one company exposed to Madagascar on CreditWatch negative because of economic risk stemming from rising institutional risks. The outlook went to stable in February 2026 in line with our rating action on Madagascar.

Rating Actions: Insurers

Our ratings on insurers are evenly split between investment and speculative grade. Our ratings on domestic insurers are underpinned by their vulnerability to local currency risk given that their assets and liabilities are concentrated in their domestic markets.

South African insurers at the highest end of the national rating scale remained unchanged in 2025 amid improving underlying creditworthiness as economic prospects in South Africa kept improving. Other South African insurers benefit from group support as they are owned by highly rated foreign parents. For example, we upgraded GIC Re South Africa Ltd. by one notch to 'BBB-' reflecting our upgrade of South Africa and our view of parent, GIC Re’s, creditworthiness. We also assigned a 'zaAAA’ national scale rating to Centriq Insurance Co. Ltd., increasing our coverage in South Africa, which has the strongest insurance penetration rate (11.5%) compared to an average of 3.0% in Africa.

In Nigeria, we raised our rating on Africa Reinsurance Corp., to 'A/Stable' from 'A-/Positive', on consistent strong operating performance and a well-established franchise across the African continent, which underpins its market-leading position. This action also led to the same rating action on its subsidiary African Reinsurance Corp. (South Africa) Ltd., which benefits from an unconditional guarantee from its parent.

Our positive outlooks reflect the positive outlook on the sovereign ratings on South Africa and would likely move in tandem with any action on the sovereign in 2026.

Appendix: Global and National Scale Rating Lists

| Africa public global and national scale sovereign ratings | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sovereign | Long-term FC rating | Short-term FC rating | Outlook | Long-term LC rating | Short-term LC rating | Outlook | National scale LT rating | |||||||||

| Angola | B- | B | Stable | B- | B | Stable | -- | |||||||||

| Benin | BB- | B | Stable | BB- | B | Stable | -- | |||||||||

| Botswana | BBB | A-2 | Negative | BBB | A-2 | Negative | -- | |||||||||

| Bank of Botswana | BBB | A-2 | Negative | BBB | A-2 | Negative | -- | |||||||||

| Burkina Faso | CCC+ | C | Stable | CCC+ | C | Stable | -- | |||||||||

| Cameroon | B- | B | Stable | B- | B | Stable | -- | |||||||||

| Cape Verde | B+ | B | Positive | B+ | B | Positive | -- | |||||||||

| Chad | B- | B | Stable | B- | B | Stable | -- | |||||||||

| Congo (the Democratic Republic of the) | B- | B | Positive | B- | B | Positive | -- | |||||||||

| Congo-Brazzaville | CCC+ | C | Stable | CCC+ | C | Stable | -- | |||||||||

| Cote d'ivoire | BB | B | Stable | BB | B | Stable | -- | |||||||||

| Egypt | B | B | Stable | B | B | Stable | -- | |||||||||

| Ethiopia | SD | SD | NM | CCC+ | C | Stable | -- | |||||||||

| Nigeria | B- | B | Positive | B- | B | Positive | ngBBB+ | |||||||||

| Ghana | B- | B | Stable | B- | B | Stable | -- | |||||||||

| Guinea | B+ | B | Stable | B+ | B | Stable | -- | |||||||||

| Kenya | B | B | Stable | B | B | Stable | -- | |||||||||

| Madagascar | B- | B | Stable | B- | B | Stable | -- | |||||||||

| Mauritius | BBB- | A-3 | Stable | BBB- | A-3 | Stable | -- | |||||||||

| Morocco | BBB- | A-3 | Stable | BBB- | A-3 | Stable | -- | |||||||||

| Mozambique | CCC+ | C | Negative | SD | SD | NM | -- | |||||||||

| Rwanda | B+ | B | Stable | B+ | B | Stable | -- | |||||||||

| Saint Helena | BBB- | A-3 | Stable | BBB- | A-3 | Stable | -- | |||||||||

| Senegal | CCC+ | C | Watch Dev | B- | B | Watch Dev | -- | |||||||||

| South Africa | BB | B | Positive | BB+ | B | Positive | zaAAA | |||||||||

| Togo | B+ | B | Stable | B+ | B | Stable | -- | |||||||||

| Uganda | B- | B | Positive | B- | B | Positive | -- | |||||||||

| Zambia | CCC+ | C | Stable | CCC+ | C | Stable | -- | |||||||||

| Note: We assign national scale ratings in Nigeria and South Africa. Our national scale ratings do not have outlook. FC--Foreign currency. LC--Local currency. LT--Long term. ST--Short term. SD--Selective default. NM--Not Meaningful. Source: S&P Global Ratings. Ratings as at Feb. 17, 2026 | ||||||||||||||||

| Africa public non sovereign and MLIs global and national scale ratings | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Entity type | Global scale LT rating | Global scale ST rating | Outlook | National scale LT rating | National scale ST rating | |||||||||

| Absa Bank Limited | Financial institution | NR | NR | -- | zaAAA | zaA-1+ | ||||||||

| Access Bank PLC | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| African Bank Ltd. | Financial institution | B+ | B | Stable | -- | -- | ||||||||

| African Development Bank | Multilateral lending institution | AAA | A-1+ | Stable | -- | -- | ||||||||

| Africa Finance Corporation | Multilateral lending institution | A | A-1 | Positive | -- | -- | ||||||||

| African Reinsurance Corp. | Insurance | A | -- | Stable | -- | -- | ||||||||

| African Reinsurance Corp. (South Africa) Ltd. | Insurance | A | -- | Stable | -- | -- | ||||||||

| African Trade & Investment Development Insurance | Multilateral Insurance Institution | A | -- | Stable | -- | -- | ||||||||

| Africell Holdings Limited | Corporate | B | -- | Stable | -- | -- | ||||||||

| AIG Life South Africa Ltd. | Insurance | BB+ | -- | Stable | zaAAA | -- | ||||||||

| AIG South Africa Ltd. | Insurance | BB+ | -- | Stable | zaAAA | -- | ||||||||

| Allianz Global Corporate and Specialty South Africa Ltd. | Insurance | BBB- | -- | Positive | zaAAA | -- | ||||||||

| AngloGold Ashanti PLC | Corporate | BB+ | NR | Positive | -- | -- | ||||||||

| Arab Bank for Economic Development in Africa | Multilateral lending institution | AA+ | A-1+ | Stable | -- | -- | ||||||||

| Arab Tunisian Bank | Financial institution | B- | B | Stable | -- | -- | ||||||||

| Attijariwafa Bank | Financial institution | BB+ | B | Stable | -- | -- | ||||||||

| Axian Telecom Holding and Management plc | Corporate | B+ | -- | Stable | -- | -- | ||||||||

| Bank of Industry Limited | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| Banque Centrale Populaire | Financial institution | BB | B | Stable | -- | -- | ||||||||

| Banque de Tunisie et des Emirats Société anonyme | Financial institution | CCC+ | C | Stable | -- | -- | ||||||||

| Banque Misr | Financial institution | B | B | Stable | -- | -- | ||||||||

| BNP Paribas Personal Finance South Africa Ltd. | Financial institution | NR | NR | NR | zaAAA | zaA-1+ | ||||||||

| Capitec Bank Ltd. | Financial institution | BB | B | Positive | zaAAA | zaA-1+ | ||||||||

| Commercial International Bank (Egypt) S.A.E. | Financial institution | B | B | Stable | -- | -- | ||||||||

| Cote d'Ivoire Energies | Corporate | BB- | -- | Stable | -- | -- | ||||||||

| Development Bank of Southern Africa Ltd. | Financial institution | BB | B | Positive | -- | -- | ||||||||

| East African Development Bank | Multilateral lending institution | A | A-1 | Stable | -- | -- | ||||||||

| Ecobank Nigeria Ltd. | Financial institution | CC | C | Negative | -- | -- | ||||||||

| Ecobank Transnational Inc. | Financial institution | B- | B | Negative | -- | -- | ||||||||

| Endeavour Mining PLC | Corporate | BB- | -- | Negative | -- | -- | ||||||||

| ESKOM Holdings SOC Ltd. | Corporate | B+ | -- | Stable | zaA | zaA-1 | ||||||||

| Exxaro Resources Ltd | Corporate | NR | NR | -- | zaA | zaA-1 | ||||||||

| FBN Holdings Plc | Financial institution | B- | B | Stable | ngBBB- | ngA-3 | ||||||||

| Fidelity Bank Plc | Financial institution | B- | B | Stable | ngBBB | ngA-2 | ||||||||

| First Bank of Nigeria Ltd. | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| First City Monument Bank | Financial institution | B- | B | Stable | ngBBB- | ngA-3 | ||||||||

| FirstRand Bank Ltd. | Financial institution | BB | B | Positive | zaAAA | zaA-1+ | ||||||||

| FirstRand Ltd. | Financial institution | B+ | B | Positive | zaA+ | zaA-1 | ||||||||

| GIC Re South Africa Ltd. | Insurance | BBB- | -- | Stable | zaAAA | -- | ||||||||

| Gold Fields Ltd. | Corporate | BBB- | A-3 | Stable | zaAAA | zaA-1+ | ||||||||

| Guaranty Trust Bank Ltd. | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| Guaranty Trust Holding Co. PLC | Financial institution | B- | -- | Stable | ngBBB- | ngA-3 | ||||||||

| Hannover Re South Africa Ltd. | Insurance | AA- | -- | Stable | -- | -- | ||||||||

| Harmony Gold Mining Company Ltd. | Corporate | BB | -- | Stable | zaAAA | -- | ||||||||

| Helios Towers PLC | Corporate | BB- | -- | Stable | -- | -- | ||||||||

| HTA Group, Ltd. | Corporate | BB- | Stable | |||||||||||

| IHS Holding Ltd. | Corporate | B+ | -- | Stable | -- | -- | ||||||||

| Investec Bank Ltd. | Financial institution | BB | B | Positive | zaAAA | zaA-1+ | ||||||||

| Ivanhoe Mines Ltd. | Corporate | B | -- | Stable | -- | -- | ||||||||

| Liberty Group Ltd. | Insurance | NR | NR | -- | zaAAA | -- | ||||||||

| Life Healthcare Group Holdings Ltd. | Corporate | NR | NR | -- | zaAAA | -- | ||||||||

| Mobile Telephone Networks Holdings Ltd. | Corporate | BB- | -- | Positive | zaAA+ | -- | ||||||||

| Morocco Upline Tresorerie. | Fund | A-f | -- | -- | -- | -- | ||||||||

| MTN Group Ltd. | Corporate | BB- | Positive | zaAA+ | -- | |||||||||

| National Bank of Egypt | Financial institution | B | B | Stable | -- | -- | ||||||||

| Nedbank Ltd. | Financial institution | BB | B | Positive | zaAAA | zaA-1+ | ||||||||

| Northern Platinum Ltd. | Corporate | BB- | -- | Stable | -- | -- | ||||||||

| OCP S.A. | Corporate | BBB- | -- | Stable | -- | -- | ||||||||

| Old Mutual Ltd. | Insurance | NR | NR | -- | zaAA+ | zaA-1+ | ||||||||

| Old Mutual Life Assurance Co. (South Africa) Ltd. | Insurance | BB+ | -- | Positive | zaAAA | zaA-1+ | ||||||||

| Petra Diamonds Ltd. | Corporate | B- | -- | Stable | -- | -- | ||||||||

| Puma International Financing S.A. | Corporate | BB | -- | Stable | -- | -- | ||||||||

| Rand Water | Corporate | BB | -- | Positive | zaAAA | -- | ||||||||

| Sanlam Ltd. | Insurance | NR | NR | -- | zaAA+ | -- | ||||||||

| Santam Ltd. | Insurance | NR | NR | -- | zaAAA | -- | ||||||||

| Sanlam Life Insurance Ltd. | Insurance | NR | NR | -- | zaAAA | -- | ||||||||

| Sanlam Capital markets | Financial institution | NR | NR | -- | zaAAA | zaA-1+ | ||||||||

| Santam SI Investments Mauritius Ltd. | Insurance | B | -- | Positive | -- | -- | ||||||||

| Santam Structured Insurance Ltd. | Insurance | BB | -- | Positive | zaAAA | -- | ||||||||

| Santam Structured Insurance Ltd. PCC | Insurance | BB- | -- | Positive | -- | -- | ||||||||

| Santam Structured Reinsurance Ltd. PCC | Insurance | BB | -- | Positive | -- | -- | ||||||||

| Sasol Ltd. | Corporate | BB+ | B | Negative | -- | -- | ||||||||

| Seplat Energy Plc | Corporate | B | -- | Positive | -- | -- | ||||||||

| Sibanye Stillwater Ltd. | Corporate | BB- | -- | Negative | zaAA- | -- | ||||||||

| Stanbic IBTC Bank PLC | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| Standard Chartered Bank Nigeria Ltd. | Financial institution | B- | B | Positive | -- | -- | ||||||||

| Super Group Ltd. | Corporate | NR | NR | -- | zaAAA | zaA-1+ | ||||||||

| Swiss Re Corporate Solutions Africa Ltd. | Insurance | NR | NR | -- | zaAAA | -- | ||||||||

| Telkom SA SOC Ltd. | Corporate | BB+ | -- | Positive | zaAAA | -- | ||||||||

| Transnet SOC Ltd. | Corporate | B+ | -- | Stable | zaA | zaA-1 | ||||||||

| Tullow Oil PLC | Corporate | CCC- | -- | Negative | -- | -- | ||||||||

| uMngeni-uThukela Water | Corporate | NR | NR | -- | zaAAA | zaA-1+ | ||||||||

| United Bank for Africa Plc | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| UPL Corp. Ltd. | Corporate | BB | -- | Stable | -- | -- | ||||||||

| Valterra Platinum Ltd. | Corporate | BBB- | A-3 | Stable | zaAAA | -- | ||||||||

| Vivo Energy Ltd. | Corporate | BB+ | -- | Positive | -- | -- | ||||||||

| Woolworths Holdings Ltd. | Corporate | NR | NR | -- | zaAAA | -- | ||||||||

| Zenith Bank Plc | Financial institution | B- | B | Positive | ngBBB+ | ngA-2 | ||||||||

| Note: We assign national scale ratings in Nigeria and South Africa. Our national scale ratings do not have an outlook. FC--Foreign currency. LC--Local currency. LT--Long term. ST--Short term. NR—Not rated. Source: S&P Global Ratings. Ratings as of Feb. 17, 2026. | ||||||||||||||

Glossary

CreditWatch: Highlights our opinion regarding the potential direction of a short-term or long-term rating. It focuses on identifiable events and short-term trends that cause ratings to be placed under special surveillance by S&P Global Ratings' analytical staff.

Issuer credit ratings: An S&P Global Ratings' issuer credit rating is a forward-looking opinion about an obligor's overall creditworthiness. This opinion focuses on the obligor's capacity and willingness to meet its financial commitments as they come due.

Fund credit quality ratings: Also known as a "bond fund rating," it is a forward-looking opinion about the overall credit quality of a fixed-income investment fund. Fund credit quality ratings, identified by the 'f' suffix, are assigned to fixed-income funds, actively or passively managed, typically exhibiting variable net asset values.

Local and foreign currency ratings: S&P Global Ratings' issuer credit ratings make a distinction between foreign currency ratings and local currency ratings. A foreign currency rating on an issuer can differ from the local currency rating on it when the obligor has a different capacity to meet its obligations denominated in its local currency versus obligations denominated in a foreign currency.

National scale rating: An opinion of an obligor's creditworthiness or overall capacity to meet specific financial obligations, relative to other issuers and issues in a given country or region.

Outlook: An S&P Global Ratings' outlook assesses the potential direction of a long-term credit rating over the intermediate term, which is generally up to two years for investment grade and generally up to one year for speculative grade. In determining a rating outlook, consideration is given to any changes in economic and/or fundamental business conditions.