Africa’s Infrastructure Funding Gap Could Put Brakes On Economic Development

While many African economies have strong economic prospects, structural constraints, including shallow capital markets, a widespread dependence on imported energy, and ongoing insufficient infrastructure investment could weigh on future growth.

S&P Global Ratings considers that those issues are often intertwined. Basic infrastructure gaps, fueled by long-term funding shortfalls, is a significant barrier to inclusive and sustainable progress. These reflect fragmented energy systems, underdeveloped transport and logistics networks, and a growing digital infrastructure gap with other regions. Together, these constrain productivity and competitiveness, limit industrial output, and hinder trade integration and connectivity across African markets.

The small size of infrastructure projects remains a key constraint to financing, with the limited scale underscoring the need for aggregation and cross-border solutions. The resultant uneven distribution of financing capacity suggests that wealth could accrue to bigger economies, while smaller economies risk falling further behind.

For example, disparity in financial maturity poses a growing risk to integrated regional infrastructure development. While larger economies, such as South Africa, Egypt, and Morocco, benefit from more developed financial systems and better access to capital markets, mid-sized and smaller economies' with often shallow financial markets limit project financing and contribute to inflated infrastructure funding costs. The resultant large and uneven infrastructure financing gap reinforces disparities in investment, economic development, while governance weaknesses can also weigh on investor appetite.

High Financing Costs, Constrained Access

Borrowing costs across African markets are high due to cyclical and structural factors--including high indebtedness, shallow domestic capital markets (see chart 1), and sparse and unreliable data. These factors can constrain market access and financial options for sovereign and sub-national entities. Furthermore, relatively large government fiscal imbalances have contributed to the deterioration of sovereign credit quality over the past two decades, driving up many African countries' debt and financing needs, typically at high costs. Finally, weak credibility and sometimes unpredictable policymaking has left many African sovereigns vulnerable to shocks, such as the COVID-19 pandemic, and to domestic political challenges.

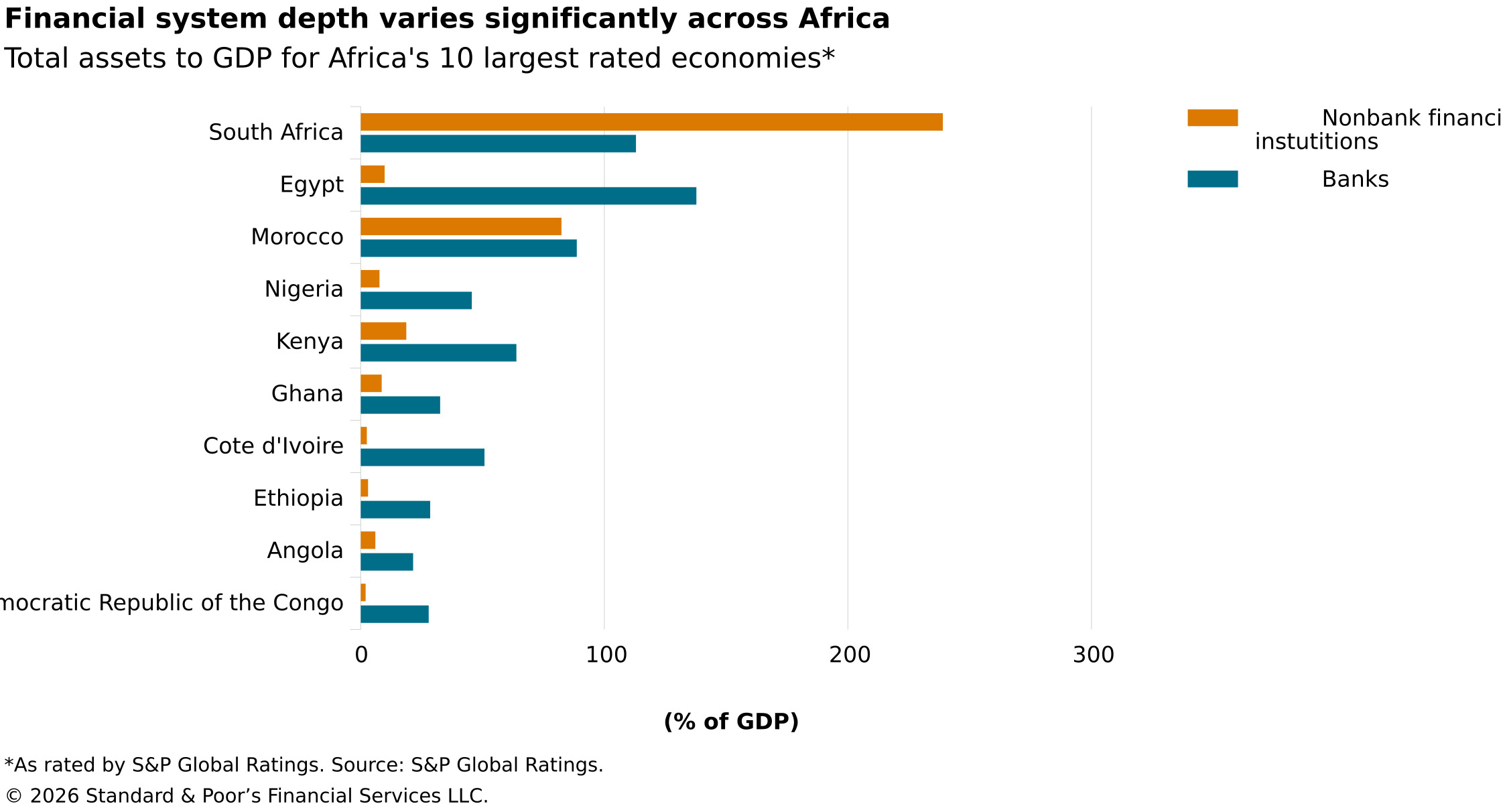

Access to financing varies by country, reflecting differences in domestic financial systems and institutional capacity. In markets with shallow financial systems, governments rely more heavily on external financing, often in foreign currency, increasing their exposure to exchange-rate volatility and debt-servicing risks—such as in Angola and Ghana. While aggregate financial assets in the largest 20 economies we rate range from 20% to more than 200% of their respective GDP, much of this capital does not flow into infrastructure investments. Instead, banks invest a large share of their assets in government bonds, limiting private-sector funding (see chart 2). For example, over 50% of banking assets in Egypt fund the government’s deficit, compared to less than 20% in developed markets. This concentration curbs the availability of resources for productive investments and limits the ability of domestic financial institutions to support large-scale infrastructure transactions.

Financial depth alone does not guarantee effective capital allocation. Limited project bankability, partly due to small transaction sizes, also limits private capital mobilization, leaving multilateral and development finance institutions to often fill a large gap in bridging financing shortfalls.

The Infrastructure Investment Gap Threatens Economic Development

African nations' combined investment in infrastructure is currently insufficient to sustain urbanization and industrialization, with current annual needs estimated at $130 billion to $170 billion. According to the Infrastructure Consortium for Africa, financing commitments rose about 30% over the last decade to almost $100 billion in 2023, supported by increased government allocations. However, the pace of investment growth (exacerbated by limited disbursement of commitments) continues to lag funding requirements, keeping the infrastructure financing gap large.

This gap puts at risk Africa’s ability to sustain growth and job creation, manage macroeconomic stability, and unlock long-term development potential. This is also compounded by the continent’s vulnerability to climate risks and extreme weather events that can damage and disrupt critical infrastructure. This risk is amplified in countries with larger net fuel import requirements, which are more exposed to ongoing energy shock from the Middle East war that can drive inflation and weaken economic growth.

The ability to close the gap by attracting institutional capital is hindered by often small and fragmented infrastructure project pipelines, emphasizing the need for greater project aggregation. Meanwhile, inefficiencies in financial intermediation constrain the deployment of domestic savings. This includes uneven pension fund development and low insurance penetration--typically below 3% of African economies' GDP, compared to a global average of 6% to 7%--which limits contractual savings, the development of a broad institutional investor base, and the pool of institutional capital available for long-term investment.

Risk Mitigation And Capital Deployment Will Be Key To Closing The Gap

Closing Africa’s infrastructure financing gap will likely require solutions that gradually address the investment risk and capital deployment constraints. We expect multilateral financial institutions will remain central partners in that process as patient and flexible providers of capital, including guarantees, risk-sharing instruments, and blended finance, especially as bilateral funding from the U.S., Europe and other countries is declining. However, the bespoke nature of the required solutions may limit their scalability.

Effectively addressing Africa's infrastructure funding shortfall will also depend on progress in deepening national capital markets and strengthening financial intermediation. Yet, even if funding becomes more readily available, the potential for improved energy, transport, and digital infrastructure will still hinge on the ability to attract capital with bankable projects. Without such progress, uneven financing flows could continue to slow Africa's efforts to close its infrastructure financing gap.