Unity-Providus Business Combination Maths: Between Expediency and Technical Financial Logic

Market intelligence information gathered by the Proshare Economic and Market Intelligence Unit (EMIU) indicates that the capital market regulatory authorities have received and approved a scheme of merger arrangement between Unity Bank Plc and Providus Bank Limited. The business combination approvals are expected to kickstart a court-ordered meeting to formalise the business combination initiated on August 6, 2024, with the formal notice from Unity Bank Plc to the NGX.

Analysts have, however, raised concerns, caveats, and interpretations around the clever or expedient accounting necessary to make the figures work for the business combination that delivered the regulatory accommodation/approval.

In the main, while the concerns are deemed - on a best-case basis, to amount to no more than a yellow flag, there is a need for further clarity, if only as a learning point on how regulatory discretion, and the arithmetic of banking combinations, work under such circumstances.

More importantly, having reviewed the scheme of arrangements for the merger, there are two which stand out readily for precedence management.

Concern 1:

Treatment of Financial Accommodation and the Incongruence of Debt as Tier 1 Capital

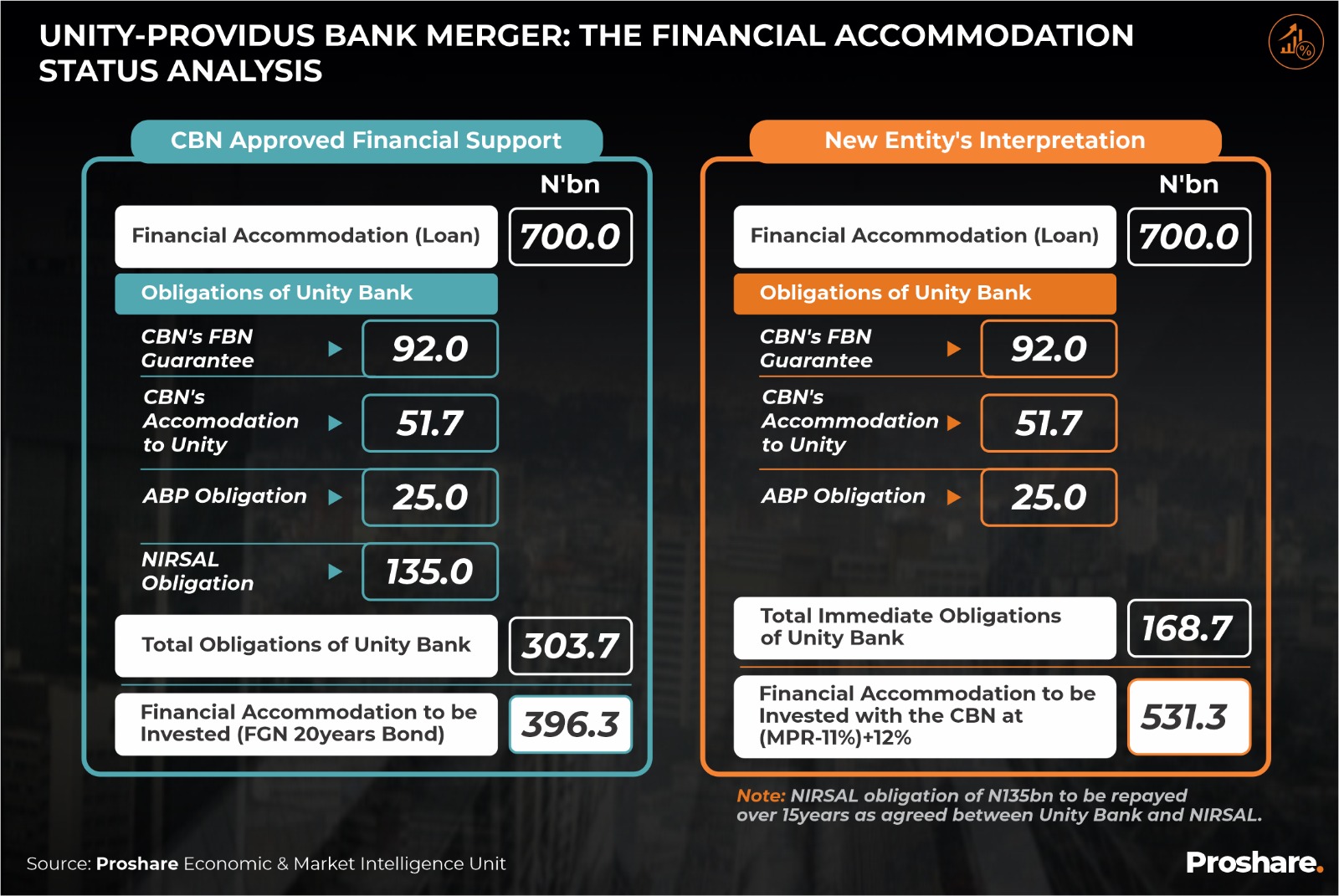

We recall the August 06, 2024, CBN Press Release announcing that the CBN had granted approval for a pivotal financial accommodation to support the proposed merger between Unity Bank and Providus Bank. We commented on this novel resolution approach in our Analyst Note on August 13, 2024, where we reviewed the structure of the financial accommodation, highlighting the incongruence between CBN’s approved accommodation of N700bn in a 20-year term loan with bond-like features. Specifically, we wondered aloud how the balance of the figure (less the obligations of Unity Bank) can be considered allowable as Tier 2 capital, given that, as structured, it is a repayable debt (see illustration 1 below).

Illustration 1:

Proshare’s EMIU’s follow-up on this viewpoint reveals that the CBN had since revised its position and approved a sum of roughly N540bn, arising from the combined entity, to be designated as Tier 1 capital.

We contend that either an error of interpretation occurred, or a redefinition of norms exists that is not widely known, as the combined entity's use of the N540bn should not pass the Tier 1 capital test. In our opinion, the very nature of Tier 1 is that it is permanent, while the nature of this CBN accommodation and the formal terms sighted thereof describe its nature as a debt that will be paid back. What entries will place a charge on equity annually?

Our EMI unit's investigation suggests that the application will fail a thorough accounting/IFRS test if subjected to globally accepted financial norms and standards, and it would indeed be interesting to see what the auditors and, indeed, the Financial Reporting Council (FRC) will say as to the designation of such debt as Tier 1 capital.

We understand that according to the Bank for International Settlements’ (BIS) BASEL to which the Nigerian Central Bank (CBN) is a signatory, “Common Equity Tier 1 capital (CET1) is the highest quality of regulatory capital, as it absorbs losses immediately when they occur. Additional Tier 1 capital (AT1) also provides loss absorption on a going-concern basis, although AT1 instruments do not meet all the criteria for CET1. For example, some debt instruments, such as perpetual contingent convertible capital instruments, may be included in AT1 but not in CET1.”

In this case, Proshare analysts argue that the CBN may have calibrated the new entity’s N540bn as ATI capital. Still, the nature of the bond-like support instrument is such that it has a 20-year maturity date that falls short of perpetuity. It should therefore not be recognised as Tier 1 capital in line with appropriate financial governance practices. We hope to learn from the clarification on the application and conventions relied on.

Concern 2:

Valuation of Plant, Property & Equipment – The Highest in the Industry

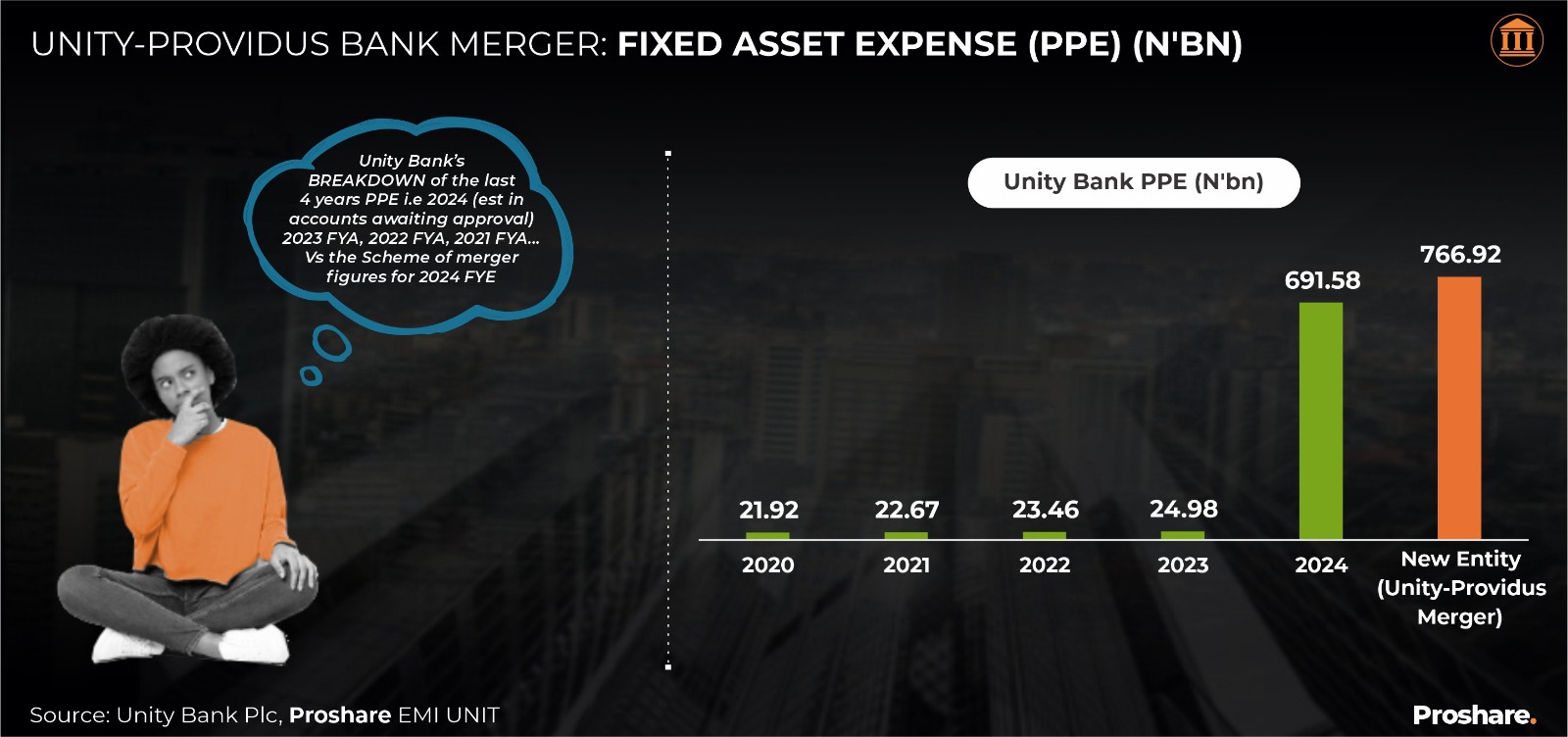

Proshare’s EMIU noted a significant increase in the Plant, Property & Equipment (PPE) value used for Unity Bank in the Scheme of Merger, rising to a figure of over N690bn from a 2023 FYE figure of N24bn, representing a 2,800% increase (see Illustration 2 below).

Illustration 2:

While we believe that the professional firm of valuers engaged by the acquiring bank will have deployed a ‘fair value’ methodology to justify this outcome, our focus is premised on the understanding, application, and stretching of IFRS 3 (Business Combinations) and IFRS 10 (Consolidated Financial Statements). Though related, they are distinct standards. While IFRS 3 and IFRS 10 both address the valuation of assets, they do so in different contexts.

Under IFRS 3, the focus is on the initial measurement of assets and liabilities acquired in a business combination, requiring them to be measured at their acquisition-date fair values.

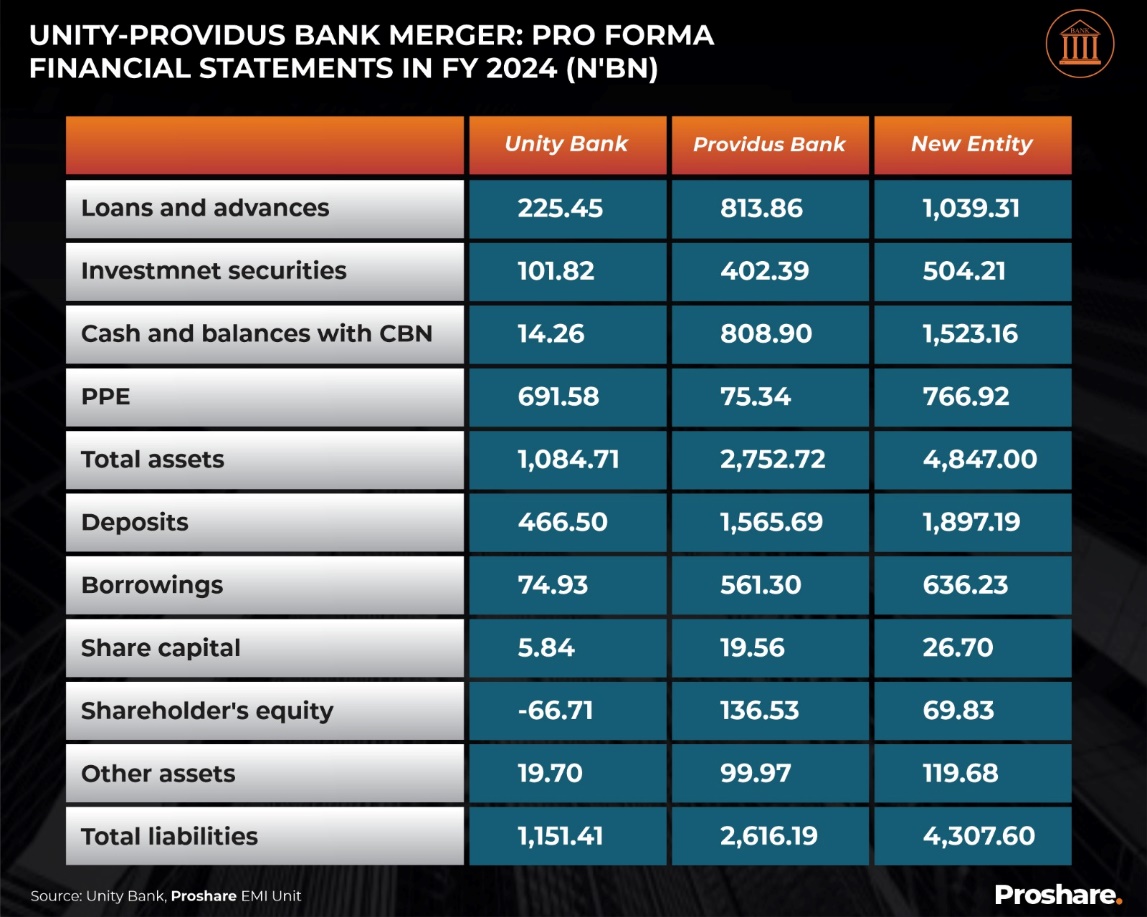

IFRS 10, on the other hand, deals with the ongoing valuation of assets within a consolidated group, including the fair value measurement of investments in subsidiaries by an investing entity (see Table 1 below).

Table 1:

For context, we undertook a comparative analysis of the Plant, Property, and Equipment (PPE) numbers for:

- Unity Bank Plc and Providus Bank over the last four (4) years, between 2020 and 2024 (as estimated in the statement of financial position awaiting approval), in other words, FYE 2024, FYA 2023, FYA 2022, FYA 2021, Vs the Scheme of merger figures for 2024FYE (see Illustration 3 below).

Illustration 3:

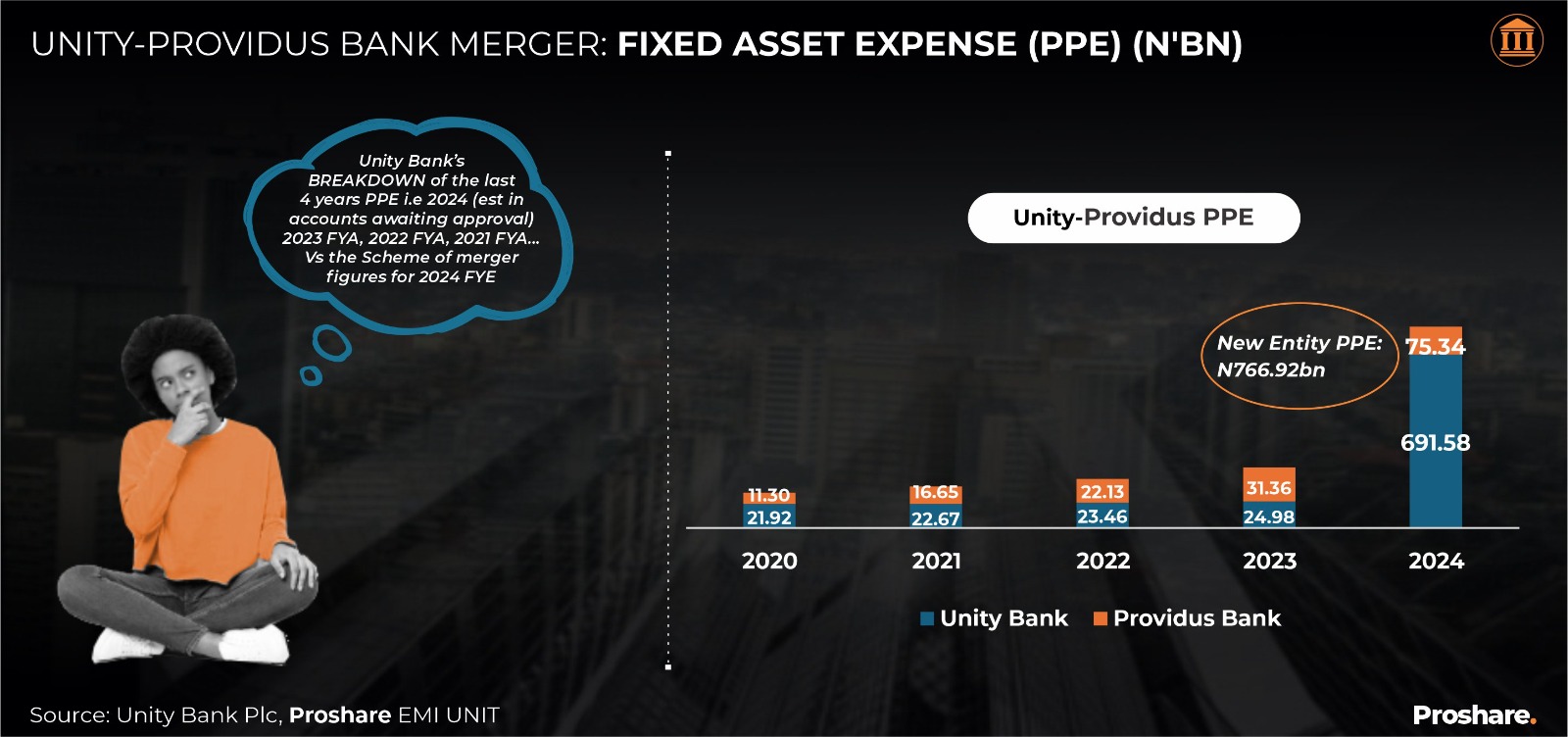

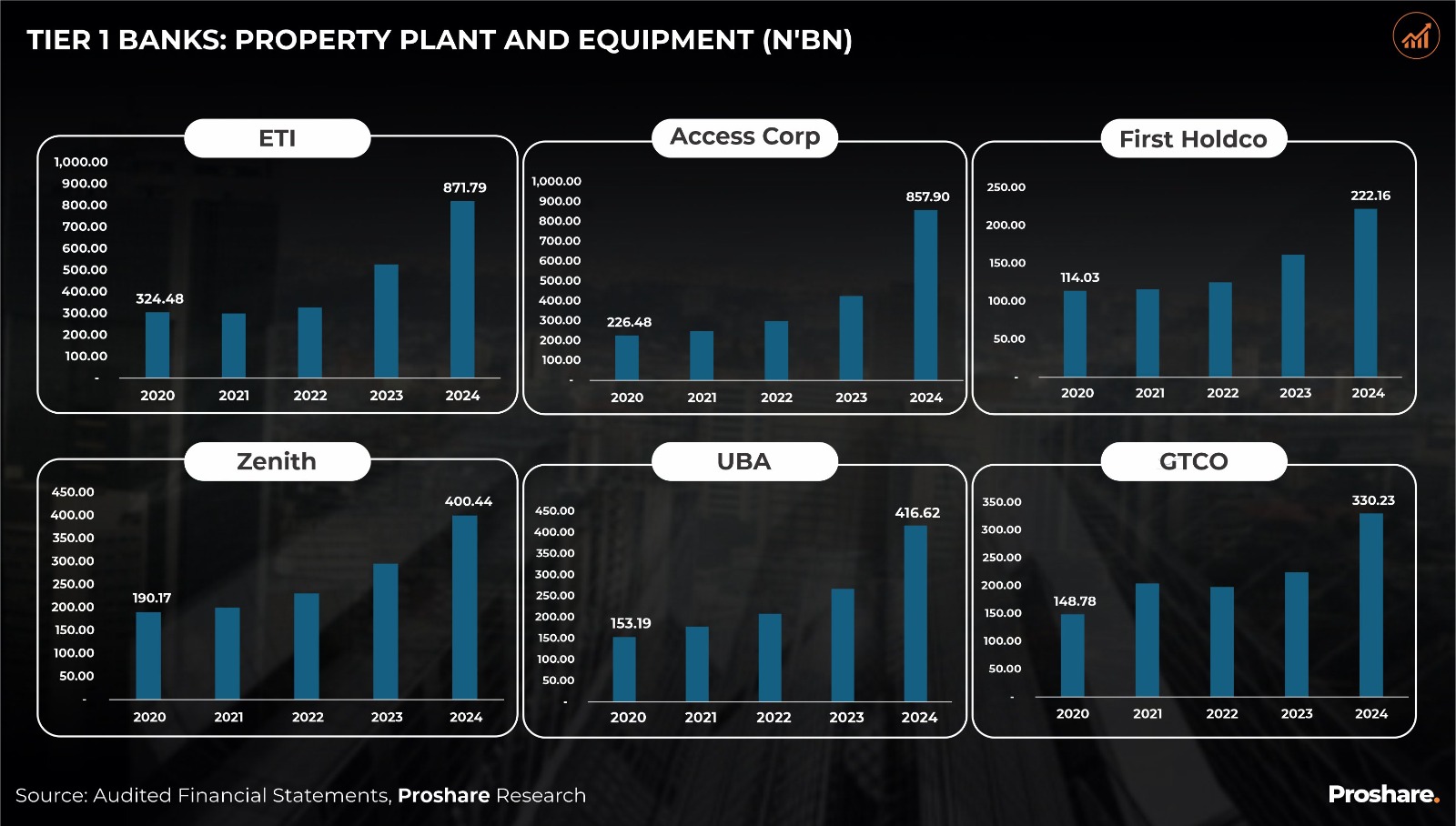

- Selected Tier 1 NGX-listed financial institutions for the years between 2020 and 2024 (see Illustration 4 below).

Illustration 4:

The findings indicated that the fair value measurement of investments (at the acquisition date) in this instance attempts to resolve the capital adequacy conundrum that exists. It is noteworthy that we did not separately explore the identification and measurement of intangible assets or goodwill that might have been present.

Validating Third-Party Thoughts

In search of clarity for future guidance on how business combinations sort out their underlying merger arithmetic, Proshare’s EMIU spoke to subject-matter experts and professionals who shared divergent but interesting perspectives.

On the CBN long-dated (20-year) Debt Instrument as Tier 1 Capital, the consensus is that this is an anomaly and aberration. According to a source, with over 35 years of banking and finance experience observed that ”the CBN and the current owners of Unity Bank may have already set a trap for the future, ironically for the new owners. There is a reason why the bank without equity capital has not been able to get fresh funding from the many suitors that approached it over the last 3 years.”

Another analyst opined, ”We should recall that when a revived New Nigeria Bank (NNB) was doing well before it merged with some illiquid banks that gave birth to the current Unity Bank, the initial outlook was grandly optimistic. After the merger, everything went sideways. I hope Providus Bank’s merger expedition will not become a similar, but avoidable, tale.”

Much Ado About PPE and Culture Clashes

The significant increase in asset valuation of Unity Bank set off several alarm bells. The leap, though explainable, has been questioned in some quarters. According to a banker who works in the Corporate Finance department of a local Lagos-based deposit money lender (DMB) and who requested anonymity, concerns about the increase in Unity Bank’s PPE are valid. ”The key stakeholders knew that the deal won’t pass without their finding a structure that will morph the debt into qualifying capital’,

‘They are at a point now where they are confident that they have a good bridge, and hence, no longer consider it to be a ‘showstopper’’. PPE revaluation surpluses are subject to regulatory restrictions to ensure such non-cash gains don’t artificially inflate capital ratios, and we expect that the CBN had scrutinised and subjected the revised valuation to rigorous due process”. Indeed, the banker upholds the view that this arrangement, if well thought through, should not be a deal breaker.

He, however, noted that “where the transaction will struggle is at the point of integration - specifically, brand and culture. Unity Bank has been positioned as the last Northern Nigeria commercial bank standing. The promoters will therefore want the combined entity to keep the Unity Bank brand even as Providus Bank is shaping up to be the surviving name (or dominant brand).

From market feedback thus far, there is justification, therefore, why the promoters of Providus Bank should be wary of repeating the mistake of Heritage Bank - where the culture of the acquired bank became the default operational mode despite the best efforts of the acquirer. And this is arguably the biggest challenge in the business combination: “How does Providus Bank ensure that it doesn’t end up being a ‘reverse takeover?”

Closing Thoughts:

The regulatory governance around the CBN’s accommodation of the Unity-Providus Bank merger appears to make fiscal adjustments that are outside normal practice. In itself, the situation is not normal – having a bank without equity capital operate for so long such that it has become inevitable that solving the problem would require regulatory ingenuity and financial creativity. The question is whether the preferred problem resolution approach adopted by CBN was the most practical and pragmatic, and at what cost to professional reporting standards and regulatory precedence?

While we acknowledge the technical validity of the arguments advanced above, we equally recognise that allowing Unity Bank to fail is not political or market expedient given its strategic importance in the northern agricultural economy and the weight of its legacy shareholders.

Our analysts contend that the most appropriate consideration of a long-dated debt instrument as part of CET1 or, at worst, AT1 Capital is if the instrument is a perpetuity (with a maturity date of 999 years as seen with instruments in countries like India) or is a debt that is convertible to equity at an agreed trigger value or period.

The current structure of the equity composition of the Unity-Providus Bank merger as presently represented:

- Falls short of the required maturity of a perpetual financial instrument.

- Does not meet the convertibility requirement, meaning that there is no principal repayment requirement as represented in the CBN 20-year maturity attached to the new bank’s bond repayment structure at a fixed coupon rate.

- Crumbles under the weight of IFRS prescription on the accounting for business combinations

- May pass the regulatory preference and guidance test that allows the regulator to independently decide on the components of CET1 and AT1 capital in line with the framework of the Bank for International Settlements (BIS) guidelines; however, this still represents a grey area of Central Banking oversight practice that requires further interrogation.

The Unity-Providus Bank business combination will undoubtedly strengthen Nigeria’s banking sector by supporting further stability and building confidence in the industry; however, fixing a crack by plastering over a house wall does not resolve the underlying foundational defect.

Finally, while the Unity Bank Plc and Providus Bank Limited merger will prove to be a significant market and institutional stabilising intervention, the lack of clarity, accounting side-stepping, and creative regulatory gymnastics suggest that the intervention cannot be replicated as a viable template for other banking combinations, given its peculiarities. We posit that regulatory discretions need to be structured to eliminate the unintended signalling of bias and fiscal indiscretion.